June 13, 2017

FHA home loans, much like their conventional counterparts, have a down payment requirement. However, unlike conventional loans, the minimum down payment requirement for FHA mortgages is 3.5% of the adjusted value of the home.

FHA home loans, much like their conventional counterparts, have a down payment requirement. However, unlike conventional loans, the minimum down payment requirement for FHA mortgages is 3.5% of the adjusted value of the home.

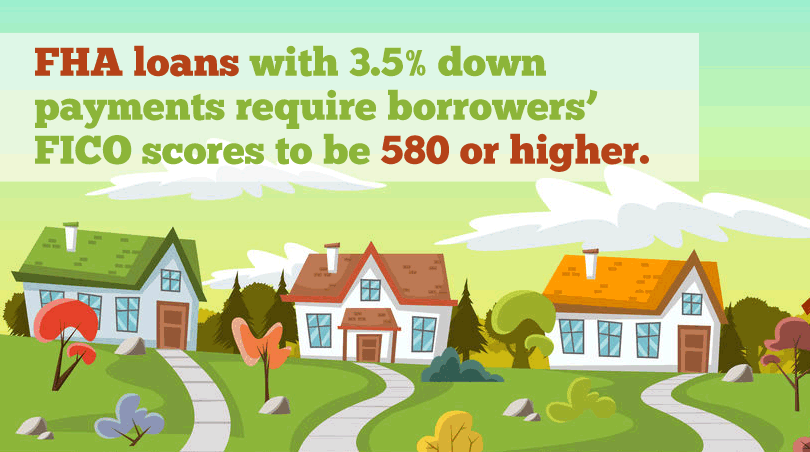

This lower down payment requirement is one of the main advantages of the FHA mortgage. The basic amount of the down payment varies with each FHA mortgage since the payment is based on the value of that particular home. Additionally, FHA mortgages require a specific FICO score range (580 or better) for maximum financing. Borrowers with FICO scores between 500 and 579 will be required to put down 10% instead of 3.5%. Additional lender standards may also apply.

Calculating the amount of your down payment is only part of the process. FHA borrowers must provide down payment money only from approved sources, and your lender will be required to verify the source of your down payment funds.

Part of the reason for this is to prevent undue influence over the loan process by interested parties-people who stand to gain from your home loan. According to HUD 4000.1, your down payment funds may not come from:

“(1) the seller of the property;

(2) any other person or Entity who financially benefits from the transaction (directly or indirectly); or

(3) anyone who is or will be reimbursed, directly or indirectly, by any party included in (1) or (2) above.”

Furthermore, while down payment funds may come from cash saved at home, savings bonds, cashed-in investments, checking account funds, or other accounts, borrowers cannot use credit card cash advances, payday loans, or third party “gifts” that are actually expected to be repaid later on. Gift funds may be permitted for down payments, but only if those gift funds are properly vetted by the lender.

The money you pay for many other costs of the loan (insurance, appraisal fees, lender fees, etc.) cannot be counted as going toward the down payment. Your minimum required down payment is an expense above and beyond the other costs of the home loan.

Talk to a loan officer to discuss the amount of a possible down payment, the sources of your down payment, and how to manage other closing costs if you aren’t sure on any of the details covered here.

Joe Wallace has been specializing in military and personal finance topics since 1995. His work has appeared on Air Force Television News, The Pentagon Channel, ABC and a variety of print and online publications. He is a 13-year Air Force veteran and a member of the Air Force Public Affairs Alumni Association. He was Managing editor for www.valoans.com for (8) years and is currently the Associate Editor for FHANewsblog.com.

Browse by Date: