September 1, 2023

How much money should a home buyer save for a down payment? The answer can’t be given in dollars and cents because the amount of your down payment depends on the purchase price of the home in part, you’ll need to know the sale price before you can calculate the down payment amount.

The percentage of the down payment (based on the price of the home) depends on the type of home loan you want, whether you want to avoid mortgage insurance, and whether your FICO scores are high enough to qualify for the lowest down payment.

Some down payment percentages are higher than others for various reasons including risk to the lender in some cases.

Down Payments For VA Mortgages

VA loans offer a no-money-down option, but there is a catch. VA loans are for service members, surviving spouses, and other qualified applicants.

You cannot purchase with a VA loan if you do not qualify for it with uniformed service, and those who do qualify cannot use a VA loan for a second home or other non-primary residences.

How Much Down Payment Is Needed For Conventional Mortgages?

The down payment on a conventional mortgage may range between 3% and 5% if you are willing to accept monthly mortgage insurance. If that is unacceptable, 20% down is typically required.

This down payment percentage is often higher when purchasing a multi-unit or second home.

Down Payments For USDA Home Loans

USDA loans feature zero-down loans for first-time home buyers and those who haven’t owed homes in a long time. However, USDA mortgages are need-based home loans and you must qualify as a person in need; income restrictions apply.

USDA loans don’t allow the purchase of investment properties or second homes. You can only purchase a primary residence with a USDA mortgage.

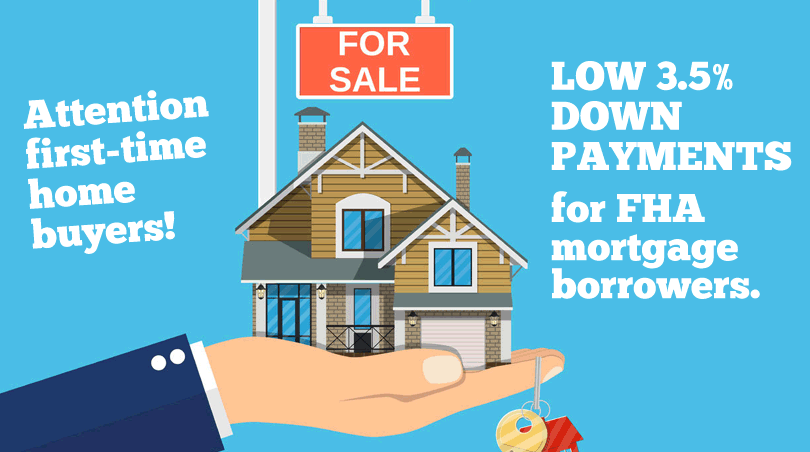

FHA Loan Down Payment Requirements

The main caveat with FHA mortgages, like other government-backed loans, is that FHA loans cannot be used for non-primary residences.

FHA borrowers agree to occupy the property purchased with an FHA mortgage. No Investment properties, second homes, or vacation homes.

These do not qualify for an FHA mortgage.

FHA loans are for all qualified borrowers, first-time buyers or not. There is a minimum required down payment for FHA loans, which is 3.5%.

One exception?

The FHA 203(h) rehabilitation loan which is meant to help those in federal disaster areas. Those rehab loans offer 100% financing and no down payment requirement, unlike other FHA mortgages.

FHA loans may require a 10% down payment in cases where the applicant’s FICO scores don’t qualify them for the 3.5% down payment. Borrowers with FICO scores 580 or higher qualify under FHA loan rules but lender requirements will also apply.

Joe Wallace has been specializing in military and personal finance topics since 1995. His work has appeared on Air Force Television News, The Pentagon Channel, ABC and a variety of print and online publications. He is a 13-year Air Force veteran and a member of the Air Force Public Affairs Alumni Association. He was Managing editor for www.valoans.com for (8) years and is currently the Associate Editor for FHANewsblog.com.

Browse by Date: